A Complete Guide for Property Buyers in Punjab & Tricity If you are planning to buy a property in Mohali, Chandigarh, Zirakpur, Panchkula or anywhere across Punjab - understanding hypothecation is not optional, it is essential.

Buyers today often explore trusted real estate platforms like Realtor.com to understand market trends, property values and home-buying insights before making a final investment decision.

Every year, thousands of property buyers across Chandigarh, Mohali, Panchkula, Ludhiana and Amritsar walk into banks, sign a stack of documents and become homeowners - yet very few truly understand what "Hypothecation" means on that loan agreement. In over two decades of working in the real estate industry across the Tricity region, I have seen how this single misunderstood term can lead to delayed property transfers, legal disputes and costly surprises at the time of resale. This guide will change that.

What Exactly is Hypothecation?

Hypothecation: A legal arrangement in which a borrower pledges an asset - in this case, a property - as collateral (security) for a loan, while retaining possession and use of that property. The lender (bank or financial institution) holds a legal charge over the property but does not take physical possession unless the borrower defaults.

In simple language: you live in your house, but the bank has a legal right over it until you repay the entire home loan. It is the invisible chain that connects your dream home to your monthly EMI.

This concept is widely used in India under the Transfer of Property Act, 1882 and the SARFAESI Act, 2002 (Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act), which gives banks the authority to seize and auction a hypothecated property in case of prolonged default - without even going to court.

Hypothecation vs. Mortgage: Know the Difference

Many property buyers in Punjab confuse hypothecation with mortgage. While both involve pledging property as collateral, they differ significantly in possession and legal rights:

Feature

Hypothecation

Mortgage

Possession of property

Remains with borrower

May transfer to lender

Common usage

Home loans, vehicle loans

Large commercial property loans

Legal framework

SARFAESI Act, 2002

Transfer of Property Act, 1882

Title of property

Stays with borrower

Can be transferred to lender

Default consequences

Bank can seize & auction

Bank enforces mortgage rights

“💡 Key Insight for Tricity BuyersWhen you take a home loan in Chandigarh, Mohali or Panchkula, what is created is a simple mortgage via hypothecation. Your property documents are deposited with the bank and a “charge” is registered in the sub-registrar's office or noted in property records - making it legally binding and publicly searchable.”

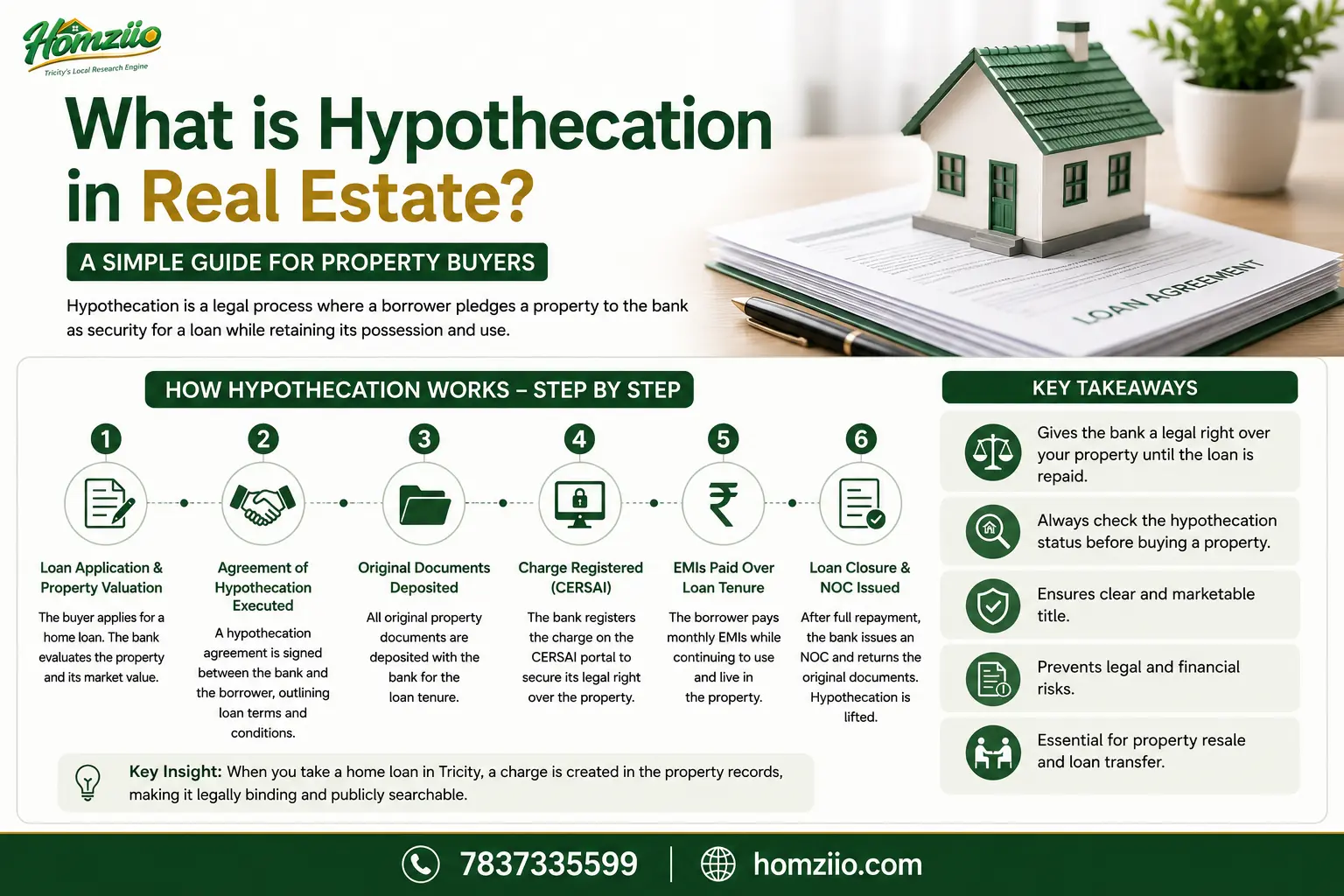

How Hypothecation Works in a Punjab Home Loan - Step by Step

Here is the exact process that unfolds when a buyer in Tricity takes a home loan:

Loan Application & Property Valuation

The buyer applies for a home loan. The bank sends its empanelled valuer to assess the market value of the property in question- be it a flat in Sector 70 Mohali or an independent house in Panchkula Sector 20.

Agreement of Hypothecation Executed

A formal "Hypothecation Agreement" is signed between the bank and the borrower. This document specifies the property address, loan amount, interest rate, tenure and the borrower's obligations.

Original Title Documents Deposited

The borrower hands over all original property documents - allotment letter, sale deed, registry, approved plans - to the bank. These are held in the bank's custody for the loan tenure.

Charge Registered (CERSAI)

The bank registers the charge on the Central Registry of Securitisation Asset Reconstruction and Security Interest (CERSAI) - an online database. This public record ensures no second loan can be taken on the same property without disclosure.

EMIs Paid Over Loan Tenure

The borrower continues to live in the property, paying monthly EMIs. The bank earns interest while holding the hypothecation charge.

Loan Closure & NOC Issued

Once the full loan is repaid, the bank issues a No Objection Certificate (NOC) and releases the original documents. The hypothecation is officially removed.

Real-Life Example from Punjab: The Mohali Flat Case

Real Case Study — Punjab

Gurpreet Singh's Flat in Mohali Sector 82, SAS Nagar

In 2019, Gurpreet Singh, a government school teacher from Ludhiana, purchased a 2BHK apartment in a GMADA-approved housing society in Sector 82, Mohali. The property was priced at ₹48 lakhs and Gurpreet availed a home loan of ₹38 lakhs from Punjab National Bank (PNB), Mohali Branch, for a 20-year tenure at 8.5% interest.

The bank executed a Hypothecation Agreement and registered the charge on CERSAI. All original documents - including the GMADA allotment letter, sale deed and occupancy certificate - were held by PNB.

In 2023, Gurpreet received a job transfer and decided to sell the property. A buyer from Panchkula expressed interest at ₹68 lakhs. However, the sale could not proceed until Gurpreet either repaid the outstanding loan (₹29 lakhs) or arranged a loan transfer (balance transfer) to the buyer's new bank, so the hypothecation could be lifted and a clear title handed over.

After negotiating with PNB and the buyer, Gurpreet arranged a foreclosure, received the NOC within 21 working days and successfully completed the sale -walking away with a net gain of approximately ₹20 lakhs after loan repayment. This is a textbook example of how hypothecation directly affects property resale timelines in Punjab.

Why Hypothecation Matters for Buyers Across Tricity

Whether you are buying a property in Zirakpur, Kharar, New Chandigarh (Mullanpur) or within Panchkula, hypothecation touches your real estate journey in multiple ways:

You cannot sell freely: A hypothecated property cannot be transferred or sold without either repaying the loan or getting explicit written consent from the bank.

Buyers check CERSAI: Informed buyers and real estate lawyers always run a CERSAI search before purchasing any resale flat or plot to check for existing charges - a must in today's Tricity secondary market.

Double-financing fraud prevention: CERSAI registration prevents fraudulent double-financing, where unscrupulous sellers take loans from two different banks on the same property - a case that has occurred in parts of Ludhiana and Amritsar in recent years.

Under-construction projects: If you are buying a flat from a builder in New Chandigarh or Mohali's Aerocity zone, check whether the land is hypothecated by the builder to a lender. If the builder defaults, your possession could be at risk.

EMI default consequences: Under the SARFAESI Act, a bank can issue a 60-day notice to a defaulting borrower and if unresolved, proceed to auction the property without a court order.

Home insurance & hypothecation: Most banks in Punjab require borrowers to take home insurance and name the bank as a co-insured party for the hypothecated property.

Removing Hypothecation - The NOC Process Explained

Once your home loan is fully repaid, removing the hypothecation is a critical step that many buyers delay-sometimes for years - without realising its long-term consequences on property title clarity. Here is how it works:

Documents You Must Collect From Your Bank

No Objection Certificate (NOC) -The most important document, confirming the bank has no further claim on the property.

Original Title Documents -All property papers deposited at loan commencement must be returned.

Deed of Receipt / Release Letter -A formal letter confirming loan closure.

CERSAI Charge Removal -Confirmation that the bank has filed for removal of the hypothecation charge on CERSAI's national database.

Encumbrance Certificate Update -Especially important in Punjab where property buyers request updated ECs from the Sub-Registrar's office, Chandigarh or respective district offices.

Common Mistake by Punjab Homeowners

Many homeowners in Panchkula, Mohali and Chandigarh repay their loans in full but never collect the NOC or get the CERSAI entry removed. When they try to sell the property 5–10 years later, the encumbrance record still shows a bank charge- creating confusion, legal delays and sometimes deal cancellations. Always collect your NOC within 30 days of loan closure.

Hypothecation in Builder-Buyer Transactions Across Punjab

In Punjab's rapidly growing residential corridors - from Aerocity Mohali to Eco City New Chandigarh and Sunny Enclave Kharar- a unique risk emerges with builder hypothecation. Many builders finance their land purchase and construction through bank loans, pledging the very land on which your apartment is being built.

Before booking a flat in any under-construction project in Tricity, always ask the builder for a written statement confirming that the land is free from any hypothecation or bank charge - or that a tripartite agreement exists between you, the builder and the bank.

-Insight from Real Estate Advisory Practice, Tricity (Est. 2004)

The Punjab Real Estate Regulatory Authority (RERA Punjab) mandates that all registered projects disclose any encumbrances on the land under RERA Act, 2016. Always verify on the RERA Punjab portal (hrera.org.in) before making your booking payment.

5 Power Tips for Smart Property Buyers in Punjab

Always run a CERSAI search before buying resale property - it costs just ₹50 online and reveals all existing charges.

Request an Encumbrance Certificate (EC) for the last 15 years from the Sub-Registrar's office of the relevant district.

If the property is under construction, insist on a Tripartite Agreement between you, the builder and the bank to protect your investment.

After full loan repayment, collect your NOC and documents within 30 days - do not let the hypothecation entry linger in records.

Verify RERA registration of your project on hrera.org.in to check for disclosed encumbrances before booking.

Always consult a local real estate professional with market knowledge of Tricity before finalising any purchase - especially in rapidly developing micro-markets like Mullanpur or Aerocity.

Hypothecation is not a scary concept- it is simply the legal backbone of every home loan in India. Understanding it empowers you to buy smarter, sell faster and protect your investment over the long term. In the Tricity real estate market - one of North India's most dynamic - where property prices in Mohali have risen by over 40% in the last four years and new corridors like New Chandigarh are redefining residential living, being an informed buyer is your greatest competitive advantage.

Whether you are a first-time home buyer in Panchkula, an NRI investor looking at Aerocity Mohal or a builder planning your next project in Punjab's growing towns - hypothecation is a term you will encounter at every step. Now you know exactly what it means and how to handle it.

Hypothecation is the pledging of your property as collateral for a home loan, where you retain possession but the bank holds a legal charge. It is created when the loan is disbursed, recorded on CERSAIand lifted upon full repayment - when the bank issues your NOC and returns your original documents. Always verify hypothecation status before buying any resale property in Punjab.

Have questions about a property in Tricity?

With over 20 years of experience serving buyers, sellers and builders across Chandigarh, Mohali and Panchkula - we are here to guide you at every step of your property journey.

Rozen Singgla is a real estate analyst and co-founder of Homziio, specialising in the Chandigarh Tricity property market. With deep expertise in RERA-verified residential and commercial projects across Mohali, Zirakpur, Kharar, and Panchkula, Rozen helps buyers and investors make informed decisions backed by verified data and on-ground market insights.

Jun 27, 2026

Jun 27, 2026 Jun 26, 2026

Jun 26, 2026 Jun 25, 2026

Jun 25, 2026