Planning to buy your dream home? Discover everything about home loans - eligibility, interest rates, EMI calculation, common mistakes and real-life tips from a real estate expert with 22+ years of experience.

I remember sitting across the table from a young couple in 2009 - Ramesh and Priya, both IT professionals from Chandigarh. They had saved every rupee for four years, dreamed of a 2BHK flat in Zirakpur and were completely overwhelmed the moment the bank handed them a 27-page loan agreement. They almost walked away. Almost.

We spent two hours that evening breaking down every clause. Today, they own not one - but two properties. And it all started with understanding how a home loan actually works.

If you are reading this, you are probably standing at a similar crossroads. The good news? You are already doing the smart thing - researching before committing.

What Exactly Is a Home Loan and Why Does It Matter?

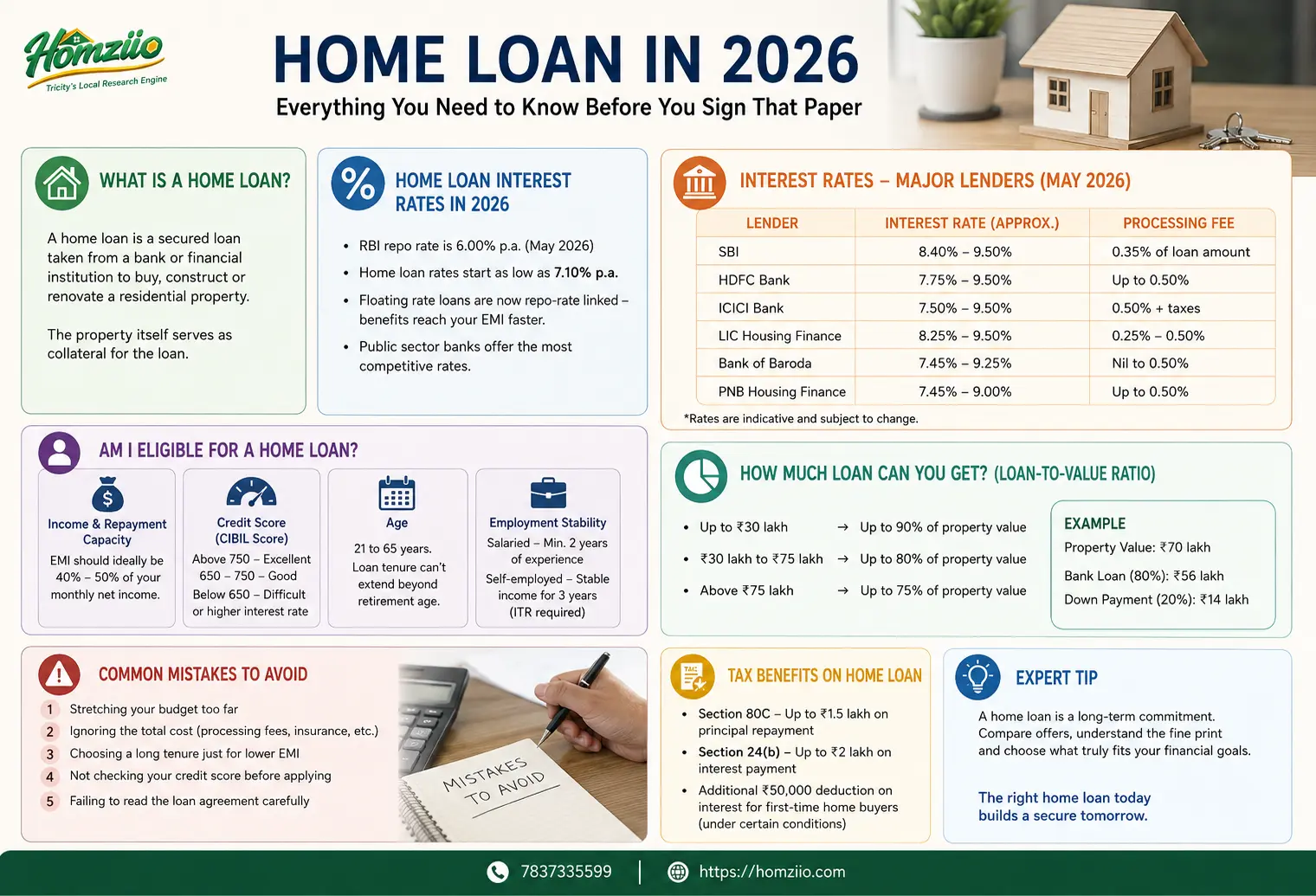

A home loan (also called a housing loan or mortgage) is a secured loan taken from a bank or financial institution to purchase, construct or renovate a residential property. The property itself serves as collateral, which is why lenders are relatively open to offering these loans compared to unsecured personal loans.

But here is what most people miss - a home loan is not just a financial product. It is a 15 to 30 year commitment that will shape your monthly budget, your tax planning and your overall financial health. Getting it right the first time matters more than most people realize.

Home Loan Interest Rates in 2026: Where Do Things Stand?

2026 has brought some welcome relief for home buyers. Following the RBI's repo rate cuts - the policy rate now sits at 6.00% per annum - most major lenders have trimmed their home loan benchmarks accordingly.

As of May 2026, home loan interest rates in India from major lenders start as low as 7.10% per annum, with the general range running between 7.45% to 9.50% depending on your credit profile, loan amount and lender.

Public sector banks like SBI, PNB and Bank of Baroda continue to lead with the most competitive rates. Private sector banks like HDFC and ICICI are slightly higher but offer faster processing and stronger digital loan journeys.

Here is a current snapshot:

Lender

Interest Rate (Approx.)

Processing Fee

SBI

8.40% – 9.50%

0.35% of loan amount

HDFC Bank

7.75% – 9.50%

Up to 0.50%

ICICI Bank

7.50% – 9.50%

0.50% + taxes

LIC Housing Finance

8.25% – 9.50%

0.25% – 0.50%

Bank of Baroda

7.45% – 9.25%

Nil to 0.50%

PNB Housing Finance

7.45% – 9.00%

Up to 0.50%

Note: Rates are indicative as of May 2026 and are subject to change based on RBI policy, borrower profile and lender discretion. Always verify current rates directly with the lender as per your query.

The most important shift in 2026 is that all floating rate home loans are now repo-rate linked (RLLR/EBLR). This means when the RBI cuts rates, the benefit reaches your EMI faster than it used to in the old MCLR era - often within the same reset cycle. This is why most financial advisors in 2026 strongly recommend floating rate loans for tenures of 15 years or more.

Am I Eligible for a Home Loan? Let's Break It Down Simply

This is the question I get asked most often. Eligibility is not complicated once you understand the four pillars that banks evaluate:

1. Income and Repayment Capacity

Banks generally allow an EMI-to-income ratio of 40% to 50%. So if your monthly net income is ₹80,000, your total EMI obligations (including the new home loan) should ideally not exceed ₹36,000 to ₹40,000.

2. Credit Score (CIBIL Score)

A CIBIL score above 750 is considered excellent and can get you the best interest rates in 2026. A score between 650–750 may still fetch you a loan but at higher rates. Below 650, most banks will hesitate or add significant risk premiums to the rate offered. The simplest way to build your score? Pay your credit card bills on time and close small outstanding loans.

Example: A client of mine - a 34-year-old teacher from Sector 80, Mohali - had a CIBIL score of 692. Three banks rejected them. We helped him clear two pending EMIs and a credit card due. Within six months, their score reached 741. He got his loan approved at 8.40% - and saved over ₹4.2 lakh in interest over the loan tenure compared to the offer he was initially getting with a weaker score.

3. Age

Most banks sanction home loans to applicants between 21 to 65 years of age. The loan tenure typically cannot extend beyond your retirement age. So a 50-year-old salaried professional may get a maximum tenure of 10–12 years, whereas a 30-year-old can opt for 25–30 years.

4. Employment Stability

Salaried individuals with at least 2 years of continuous employment (1 year with the current employer) are preferred. Self-employed professionals need to show a stable income for at least 3 consecutive financial years through ITR filings.

How Much Loan Can You Actually Get?

Banks in India typically finance 75% to 90% of the property value (called Loan-to-Value or LTV ratio) depending on the loan amount:

Loans up to ₹30 lakh → Up to 90% LTV

Loans between ₹30 lakh to ₹75 lakh → Up to 80% LTV

Loans above ₹75 lakh → Up to 75% LTV

This means if you are buying a property worth ₹70 lakh, the bank will fund ₹56 lakh. The remaining ₹14 lakh (20%) is your down payment - which you need to arrange independently.

Pro Tip from my 22 years of experience: Never stretch your down payment to the point where you are left with zero liquidity. I have seen families take out personal loans for the down payment and then struggle for 3 years with double EMIs. Keep at least 3–6 months of expenses as an emergency buffer even after the down payment.

The Home Loan Process: Step by Step

Getting a home loan approved is not as daunting as it looks. In 2026, most lenders have significantly digitized the process and approvals can come faster than ever. Here is the process simplified:

Step 1 – Calculate your eligibility using your income, existing EMIs and credit score. Use any bank's online EMI calculator for a rough estimate before you even walk into a branch.

Step 2 – Compare lenders - do not just walk into your salary account bank. Spend an afternoon comparing at least 4–5 lenders on rates, processing fees, prepayment charges and customer service reputation. In 2026, platforms like BankBazaar and Paisabazaar make this comparison straightforward.

Step 3 – Submit documents. The standard checklist includes: identity proof (Aadhaar/PAN), address proof, income proof (salary slips/ITR for last 2–3 years), bank statements for the last 6 months, property documents and photographs.

Step 4 – Property legal and technical verification. The bank will send its own legal team and a technical evaluator to verify the property's title documents and assess its construction quality and market value.

Step 5 – Loan sanction and disbursement. Once everything checks out, you get the sanction letter. Disbursement happens in stages for under-construction properties and in one go for ready-to-move properties.

The entire process typically takes 7 to 21 working days depending on the lender and the complexity of property documentation.

5 Major Mistakes First-Time Home Loan Borrowers Make

In over two decades of guiding home buyers, I have seen the same mistakes come up repeatedly. Here are the five that cost people the most:

Mistake 1: Not checking the credit score before applying. Every loan application creates a "hard inquiry" on your credit report, which slightly dips your CIBIL score. Applying to 6 banks simultaneously can hurt your score and reduce your chances of approval. Always check your score first - use free tools from CIBIL, Experian, or your bank's app and then apply selectively.

Mistake 2: Ignoring the fine print on prepayment charges. Many borrowers do not read prepayment clauses. RBI has banned prepayment penalties on floating rate loans, but fixed rate loans may still carry charges of 2–3% on the outstanding principal. In 2026, with rates on a downward trend, the ability to prepay freely is more valuable than ever.

Mistake 3: Choosing the longest tenure just to get a lower EMI. A ₹55 lakh loan at 8.50% for 30 years will cost you over ₹1.05 crore in total interest alone. The same loan for 20 years will cost approximately ₹62 lakh in interest - a saving of over ₹43 lakh. If you can afford slightly higher EMIs, shorter tenures save a fortune.

Mistake 4: Not considering home loan insurance. Life is unpredictable. A reducing-term home loan insurance policy in 2026 costs roughly ₹9,000–₹18,000 per year depending on the loan size and your age. It ensures your family is never forced to sell the home if something happens to you. It is one of the most underrated financial decisions a home buyer can make.

Mistake 5: Buying property without verifying the title. This is where I strongly urge every buyer - never skip independent legal verification. Banks do check title documents, but their primary concern is their own security, not yours. Always hire your own property lawyer for a title search. The fee of ₹5,000–₹15,000 for a proper legal opinion can save you from disputes worth lakhs.

Tax Benefits on Home Loan in 2026 - A Smart Borrower's Advantage

One of the most underutilized benefits of a home loan in India remains the tax deduction under the Income Tax Act. Even in 2026, for those choosing the Old Tax Regime, the benefits are substantial:

Section 80C: Deduction of up to ₹1.5 lakh per year on principal repayment

Section 24(b): Deduction of up to ₹2 lakh per year on interest paid (for self-occupied property)

Section 80EEA: Additional ₹1.5 lakh deduction for first-time buyers on affordable housing (subject to property value and stamp duty conditions)

Important note for 2026: If you have opted for the New Tax Regime, deductions under 80C and 80EEA are not available. However, Section 24(b) interest deduction applies only under the Old Regime. This is a critical point many borrowers miss when switching tax regimes - always consult a CA before making your regime choice if you have a home loan.

For a borrower in the 30% tax bracket under the Old Regime, paying ₹3.5 lakh in annual interest, this translates into a real tax saving of roughly ₹60,000 to ₹70,000 per year. Over a 20-year loan, that is a significant amount back in your pocket.

2026 Market Context: Why This Is Actually a Good Time to Buy

In my 22 years in real estate, I have seen multiple cycles - the post-2008 slowdown, the demonetization dip of 2016, the COVID disruptions and the rate hike era of 2023–2024. What I am seeing in 2026 is a more stable and buyer-friendly environment than we have had in quite some time.

The RBI has been on a rate-cutting path. Property prices in Tier 2 cities like Chandigarh, Jaipur and Lucknow have appreciated 12–18% in the last two years, but there is still room before they become unaffordable. Inventory for ready-to-move homes has improved significantly and lenders are competing aggressively - processing times are shorter, documentation has been digitized and pre-approved loan offers are more accessible than ever.

If you have been sitting on the fence about buying, the combination of easing rates, growing inventory and improving digital loan processes in 2026 makes a compelling case to move forward - thoughtfully and with full preparation.

Final Thoughts: The Right Home Loan Is the One That Fits Your Life

After guiding hundreds of families - from young couples buying their very first 1BHK to NRIs investing in premium villas - I have come to one consistent conclusion: the best home loan is not always the one with the lowest interest rate. It is the one that aligns with your income, your future plans, your prepayment potential and your peace of mind.

Take your time. Compare well and never hesitate to ask questions - even the ones that feel basic. In real estate, the "basic" question is often the one that saves you lakhs.

If you have any specific questions about home loans or property buying in your city, feel free to reach out through the contact form below. I am always happy to help guide you - just like I did for Ramesh and Priya back in 2009.

“Disclaimer: Interest rates and figures mentioned are indicative as of May 2026. Always verify current rates directly with lenders before making financial decisions. Tax benefit information is subject to prevailing Income Tax rules - consult our Real Estate experts for personalised advice.”

Rozen Singgla is a real estate analyst and co-founder of Homziio, specialising in the Chandigarh Tricity property market. With deep expertise in RERA-verified residential and commercial projects across Mohali, Zirakpur, Kharar, and Panchkula, Rozen helps buyers and investors make informed decisions backed by verified data and on-ground market insights.

Jun 28, 2026

Jun 28, 2026 Jun 27, 2026

Jun 27, 2026 Jun 26, 2026

Jun 26, 2026